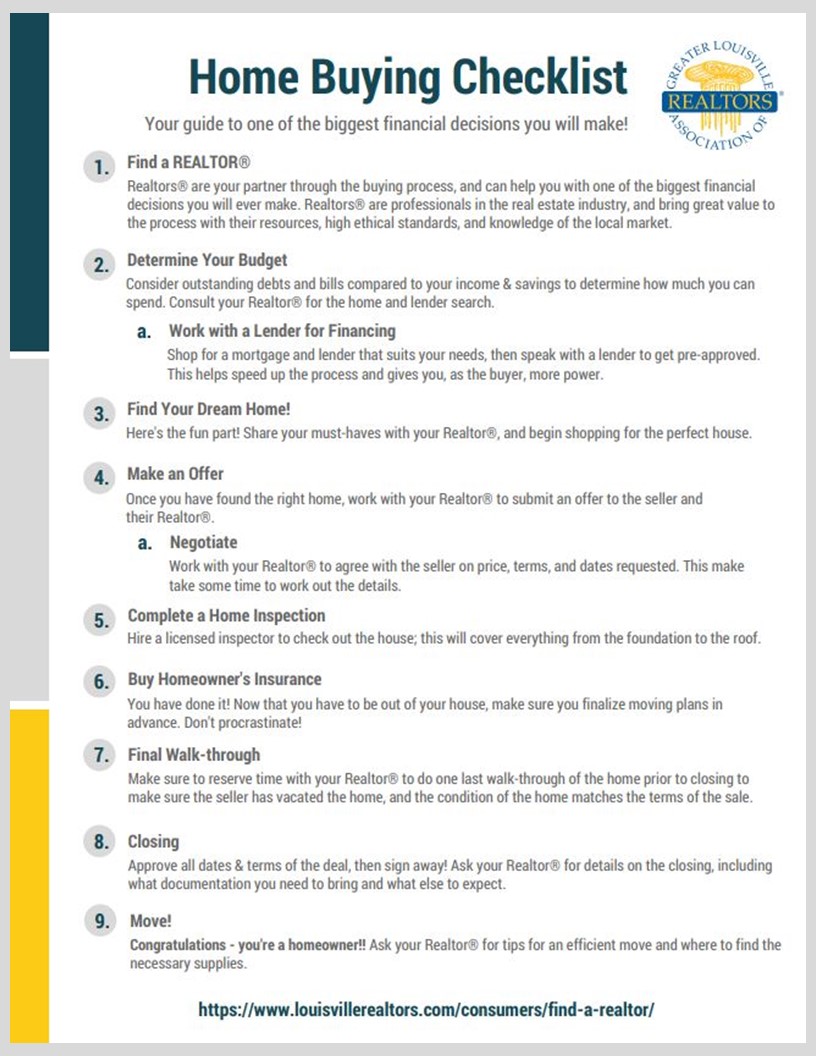

One of the first steps to take when buying a home is to establish a home purchasing budget. A budget serves as the basis for the home search, from location to size to home model. This will save you time. With a budget in mind, a REALTOR can quickly identify homes that will properly meet your needs. Your REALTOR can also assist you in determining your budget.

The next step in becoming a serious home shopper is getting pre-approved for a mortgage loan. Now that you’ve chosen your REALTOR, ask them what lenders they recommend. Nearly 9 out of 10 homes are purchased with financing, so a REALTOR will know plenty of lenders. Lenders may be a bank, mortgage company, credit union, or private lender. Having pre-approval means a loan officer has run a credit check, reviewed credit history and believes the buyer can be approved for a loan almost instantly. Besides speeding up the shopping and closing process, this makes the financial transaction easier and less stressful. Contact a REALTOR or lender to get pre-approved today.

Now that you have chosen the right REALTOR, it is time to shop for the right mortgage. Start with places where you have been pre-approved or your traditional bank where your checking and savings accounts are held.

Make sure that you and the lending company have investigated all options, whether that includes an FHA first-time homebuyer’s credit or shorter-term loan with lower interest rates. Remember, not all loan companies’ standards are the same, so if rejection comes from one company, another may approve you. Your REALTOR can also provide you with professional guidance.

The Federal Fair Housing Act prohibits discrimination in housing sales or loans on the basis of race, religion, color, national origin, sex, familial status (having children under the age of 18), or handicap.

With a budget in mind, create a wants and needs list. While a million-dollar mansion may be the dream, it is essential to differentiate between what you really need versus what you simply want. Start with decisions like what part of town, whether you want a newer or older home, a large plot of land or little yard. Then decide what features you really need. List these answers in order of importance and keep the list handy while shopping for homes. Share this list with your REALTOR so everyone is on the same page.

Once you have selected the appropriate home features, hit the streets and find out what’s out there. Call your REALTOR to get a selection of homes that fit your specifications. Ask your REALTOR to start your home search based on your preference of location, size, or price. Once they have the details, they can quickly pull together a list of appropriate properties.

Once your perfect home has been decided upon, it’s time to make the offer. An offer is a legally binding written document. However, this is not the end of the sale. A seller has the right to accept, counter or even decline the offer. Even if accepted, the purchase must still close.

Before submitting the offer, ask your REALTOR to prepare a Comparative Market Analysis (CMA). This provides you with a tool to compare similar prices that homes have sold for in the area. Your REALTOR will prepare the offer, as they have the expertise to make the transaction easier. The offer includes the basic terms including the purchase price and method of payment. Other provisions of the offer include time frame and inspections.

When it comes time to make an offer on your dream home, ask your REALTOR for assistance. They are the experts and can facilitate the negotiations in a way that is beneficial to you.

The home inspection can be one of the most important facets of closing on a home. Anticipating a clean bill of health during the inspection can be the most nerve-wracking part of the process for both the buyer and the seller. Fortunately, your REALTOR knows what to do, which helps keep stress levels down during this time. Most purchase agreements hinge on the final inspection.

A typical home inspection covers the home’s heating and central air system; interior plumbing and electrical systems; the roof, attic and visible insulation; walls, ceilings, floors, windows and doors; the foundation, basement and structural components.

To find a trusted home inspector near you, contact your REALTOR.

A typical home inspection covers the home’s heating and central air system; interior plumbing and electrical systems; the roof, attic and visible insulation; walls, ceilings, floors, windows and doors; the foundation, basement and structural components.

To find a trusted home inspector near you, contact your REALTOR.

Before submitting the offer, ask your REALTOR to prepare a Comparative Market Analysis (CMA). This provides you with a tool to compare similar prices that homes have sold for in the area. Your REALTOR will prepare the offer, as they have the expertise to make the transaction easier. The offer includes the basic terms including the purchase price and method of payment. Other provisions of the offer include time frame and inspections.

When it comes time to make an offer on your dream home, ask your REALTOR for assistance. They are the experts and can facilitate the negotiations in a way that is beneficial to you.

This is the paperwork part of the process, so prepare your John Hancock. Take all of the papers you have to the closing, from the good-faith estimate to the inspector’s report. You’re typically entitled to a 24-hour, pre-closing walk-through to ensure the home is in the agreed condition. The buyer’s participation in closing includes the legal side, signing documents agreeing to transfer ownership and the lending terms.

People who may attend:

Attorney/closing agent

The buyer and seller

REALTORS from both the buyer and the seller

A representative of the lender

Closing documents you’ll need to complete the sale and move in:

HUD-1 Settlement Statement

Final Truth in Lending Statement

Mortgage note

Mortgage

Certificate of Occupancy (only on newly constructed homes)

Congratulations, you are now a new homeowner!

At the closing, the new homeowner must prove at least minimum coverage for the house. A lender’s collateral is the house, and they will not sign off on a purchase without knowing it is covered. This will be stated in the HUD-1 form that is presented at closing.

Title insurance covers issues such as unpaid property taxes, liens and other issues from previous owners. Any lender will require this insurance throughout the life of the loan.